According to the latest announcement made by the Monetary Policy Committee’s (MPC) of the Reserve Bank, debt holders face higher home loan repayments. The repo rate climbs by another 75 basis points to 5.5% per annum, ultimately pushing the prime lending rate to 9%.

Tribune South Africa reports that according to Reserve Bank governor, Lesetja Kganyago, the sizeable hike is due to the current view of inflation risks, and comes a day after Statistics South Africa published the latest headline inflation figure. The inflation rate reached 7.4% in June, the highest level since the global financial crisis and well above the 6% ceiling of the central bank’s target range.

Harcourts South Africa’s Chief Executive Officer, Richard Gray, says “Although we had our suspicions there would be a hike, this is the highest increase in almost 20 years. It is disappointing that the SARB is choosing to raise interest rates as a counter to inflation when the real reason for the high inflation is the fuel price and not consumers overspending.”

Also read: South Africa’s triple threat: loadshedding, petrol price and electricity tariffs

Many economists and analysts who forecasted an increase of 50 basis points were shocked to hear the steep rate hike. Unsurprised, however, was Regional Director and Chief Executive Officer for RE/MAX of Southern Africa, Adrian Goslett who says that he is interested to see whether this latest hike will affect activity within the local housing market.

“In the first quarter of the year, we already noticed activity subside following the first interest rate hike that was announced in November 2021. However, housing market activity inexplicably bounced back in Q2 and is now even stronger than it was last year,” he explains.

“While I do expect that buyer activity will take a knock following this latest hike, I am also optimistic that demand for real estate will remain strong. Interest rates are still roughly 1% lower than pre-pandemic levels and the housing market was still active when the prime was at around 10% pre-COVID. Even after this latest interest rate hike, it is still more affordable to take out a home loan now than it was back in 2020, which leads me to believe that the property market will remain active despite the increasing interest rates,” says Goslett.

“It is difficult to say what lies ahead for the local housing market. My advice is to prepare for the worst and to expect the best. For buyers and tenants, this means leaving room in the budget for future interest rate hikes. For sellers and landlords, this means setting a fair asking price and rental amount so that buyers and tenants are able to afford the purchase and the rent. For agents, this means building up savings to get you through quiet months with no sales. It is always better to be well prepared and not need it than to be unprepared when disaster strikes,” he concludes.

Goslett’s advice to buyers over this time is to make use of the various online affordability calculators to work out what the repayments will be at higher interest rates before going ahead with a purchase.

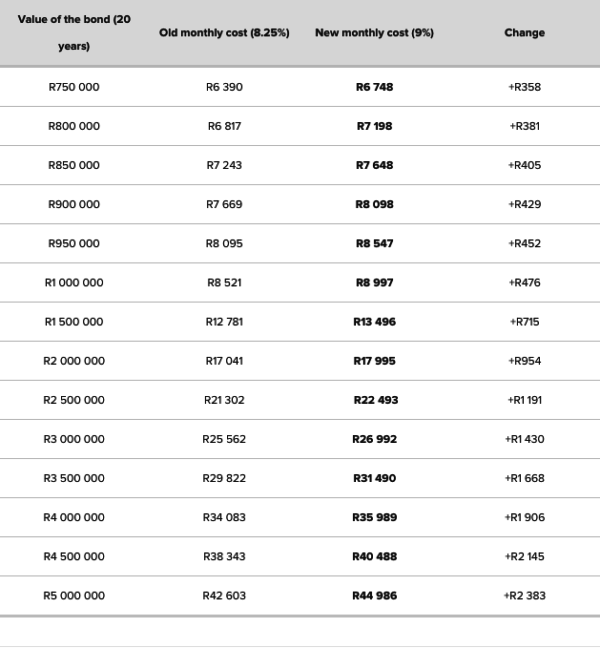

The table below from BusinessTech outlines what you can expect to now pay on your bond each month, following the rate hike:

Also read:

The cost of Eskom grid customers using solar power? R938 per month

Picture: Unsplash